In the world of finance, effective planning and decision-making are paramount. Two fundamental tools that play a pivotal role in this process are budgeting and forecasting. These tools are crucial for individuals, businesses, and organizations looking to manage their finances wisely and achieve their financial goals. In this comprehensive guide, we will explore what budgeting and forecasting are, how they differ, and why they are essential components of financial management.

Budgeting: The Financial Roadmap

What is Budgeting?

At its core, budgeting is the process of creating a detailed financial plan for a specific period, often spanning from a month to a year or more. This plan, known as a budget, serves as a financial roadmap, outlining expected income, expenses, and savings. Budgeting enables individuals and organizations to allocate resources efficiently and make informed financial decisions.

The Purpose of Budgeting

1. Control Spending

One of the primary purposes of budgeting is to control spending. By setting limits on various expense categories, individuals and businesses can prevent overspending and maintain financial discipline.

2. Goal Setting

Budgets are powerful tools for setting and achieving financial goals. Whether it’s saving for a down payment on a house, paying off debt, or funding a dream vacation, a budget helps allocate resources toward these objectives.

3. Financial Awareness

Budgets promote financial awareness by requiring meticulous tracking of income and expenses. This heightened awareness can lead to better financial decision-making and a deeper understanding of one’s financial habits.

4. Crisis Preparedness

Having a budget in place acts as a financial safety net during unexpected crises. It helps identify areas where expenses can be reduced if the need arises, providing a sense of financial security.

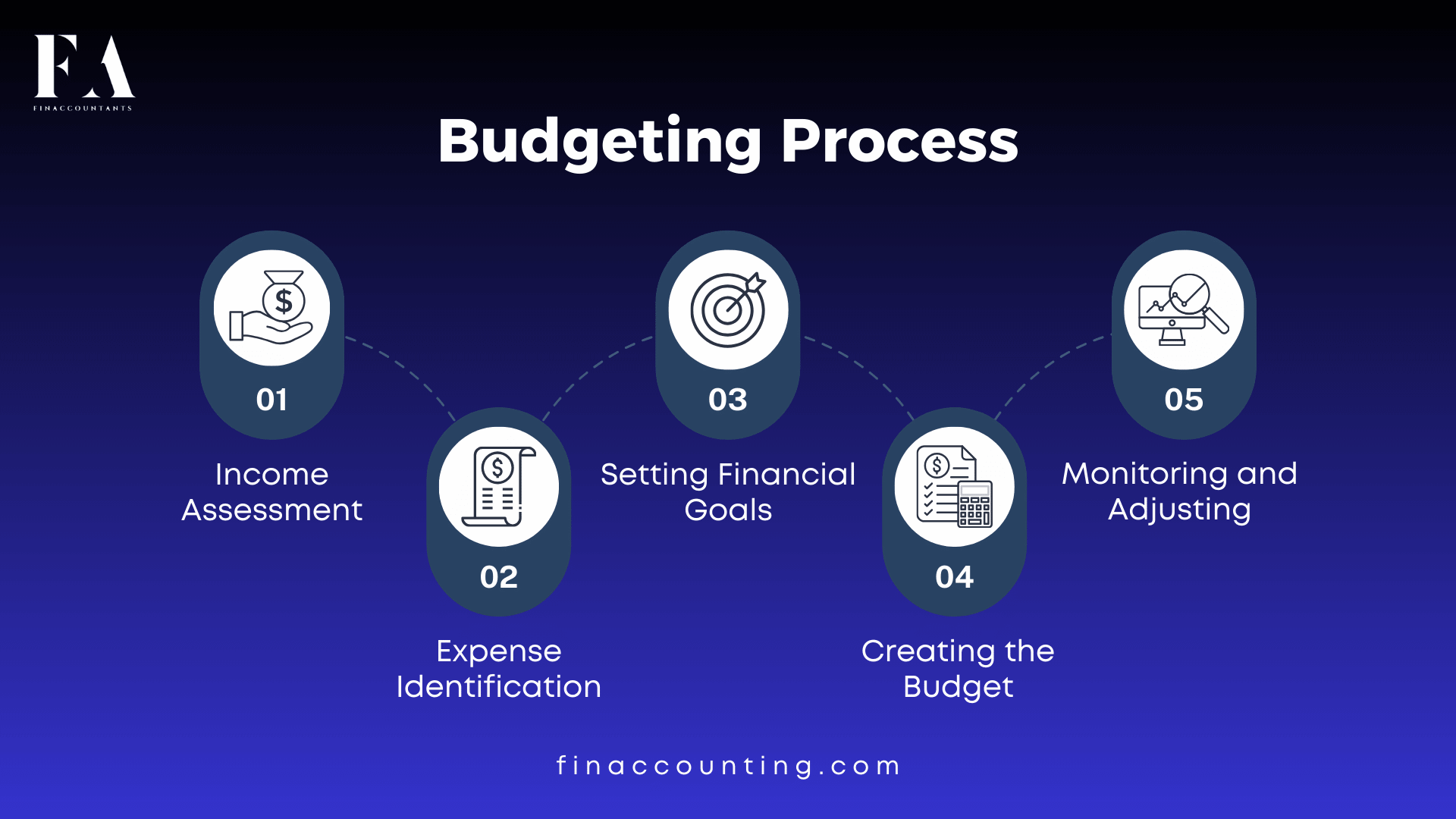

The Budgeting Process

Creating a budget involves several key steps:

1. Income Assessment

Start by determining all sources of income, including salaries, rental income, investment returns, and any other inflows of money.

2. Expense Identification

Categorize expenses into fixed and variable categories. Fixed expenses, such as rent or mortgage payments, typically remain constant, while variable expenses, like groceries or entertainment, can fluctuate.

3. Setting Financial Goals

Define both short-term and long-term financial goals. These could range from paying off credit card debt within a year to saving for retirement over the course of a few decades.

4. Creating the Budget

Allocate your income to various expense categories and savings goals. The key is to ensure that expenses do not exceed income, allowing for both savings and covering essential costs.

5. Monitoring and Adjusting

Regularly track your actual spending against the budget. If you find discrepancies or changes in your financial situation, be prepared to make adjustments to your budget accordingly.

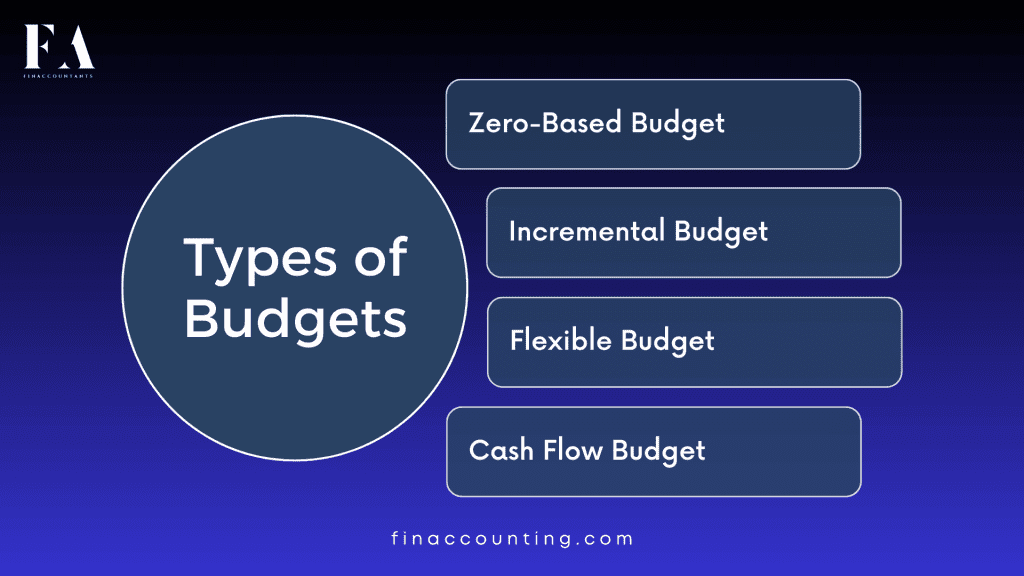

Types of Budgets

Budgets come in various forms, each tailored to specific needs and preferences. Here are some common types:

1. Zero-Based Budget

In a zero-based budget, every dollar is allocated to an expense or savings category, leaving no room for unallocated funds. This approach encourages a high level of financial accountability.

2. Incremental Budget

An incremental budget is based on the previous period’s budget, with minor adjustments. It is less time-consuming but may not be as precise as other budgeting methods.

3. Flexible Budget

Flexible budgets allow for adjustments as income and expenses fluctuate. This flexibility is especially valuable for businesses with variable revenues.

4. Cash Flow Budget

Cash flow budgets focus on tracking and managing cash flows, particularly for businesses. They help ensure there is enough liquidity to cover expenses, making them essential for cash-dependent operations.

Forecasting: Peering into the Financial Crystal Ball

Forecasting, on the other hand, is the process of making predictions or estimates about future financial outcomes. It relies on analysing historical data, current trends, and various data sources to project what is likely to happen financially in the future. While budgeting focuses on planning and control, forecasting is about anticipating what may occur.

The Purpose of Forecasting

1. Strategic Planning

Forecasts are indispensable for strategic planning. They provide insights into future market conditions, revenue projections, and potential expenses, helping businesses make informed decisions.

2. Resource Allocation

Accurate forecasts enable the efficient allocation of resources. For instance, a manufacturing company can adjust production levels based on forecasted demand, minimizing waste and maximizing efficiency.

3. Risk Management

Forecasts can identify potential financial risks and uncertainties, allowing organizations to prepare for adverse scenarios. Being forewarned about financial challenges enables proactive risk management.

4. Investor Relations

Companies often use financial forecasts to communicate their growth potential to investors and stakeholders. Reliable forecasts can instill confidence and attract investment.

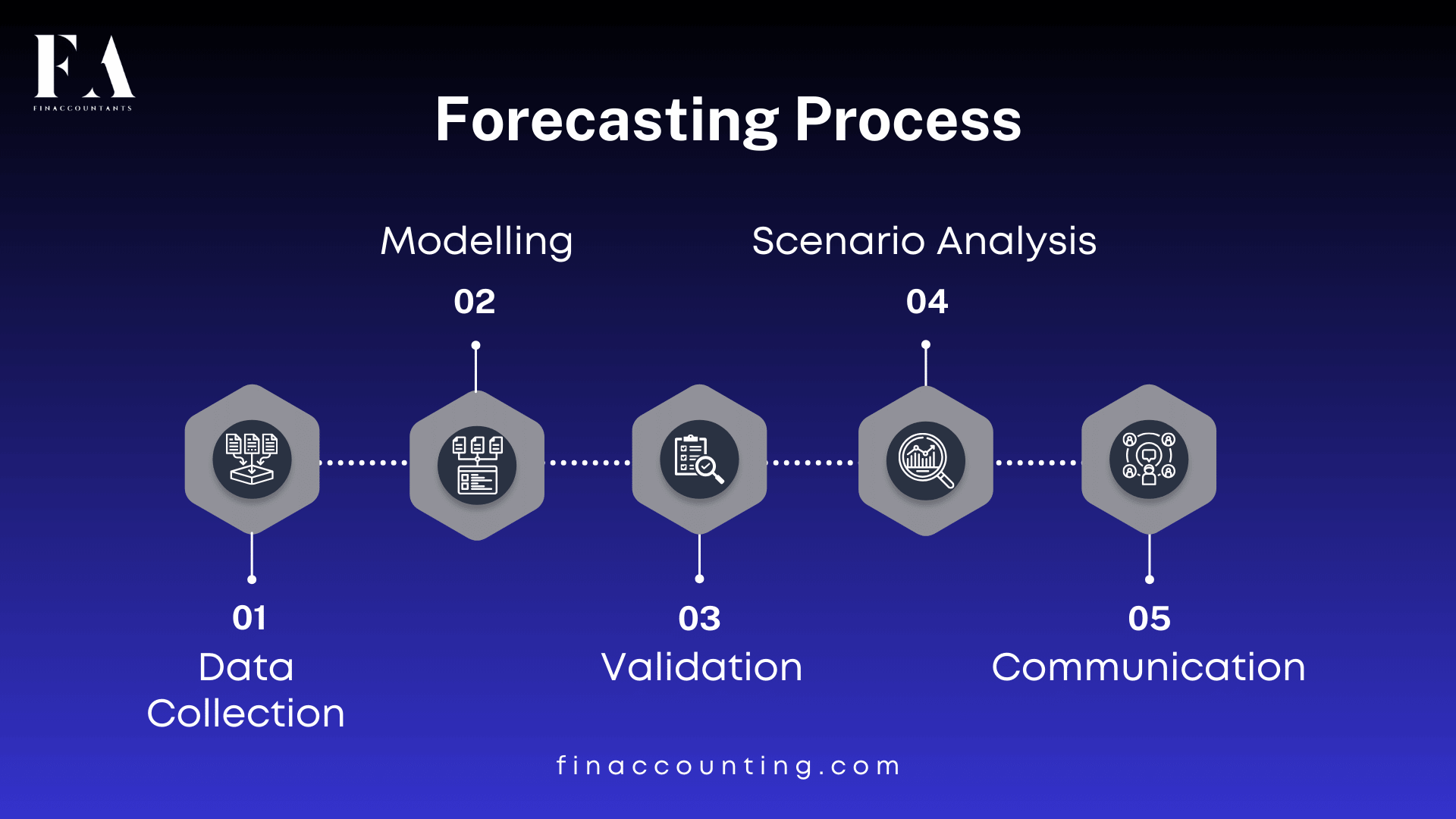

The Forecasting Process

Creating a financial forecast involves several crucial steps:

1. Data Collection

Gather historical financial data, market trends, economic indicators, and any other relevant information. The quality and accuracy of data are essential for robust forecasts.

2. Modelling

Use statistical methods, financial models, and software tools to analyse the data and generate forecasts. The complexity of the modelling process can vary widely depending on the forecasting goals.

3. Validation

It’s critical to validate the accuracy of forecasts by comparing them to actual results from the past. This step helps refine forecasting models and improve future predictions.

4. Scenario Analysis

Forecasts should consider multiple scenarios, including best-case, worst-case, and most likely outcomes. This approach accounts for uncertainties and prepares organizations for various eventualities.

5. Communication

Share the forecasts with relevant stakeholders, such as management, investors, and financial analysts. Clear communication of forecasted financial performance is essential for decision-making and investor relations.

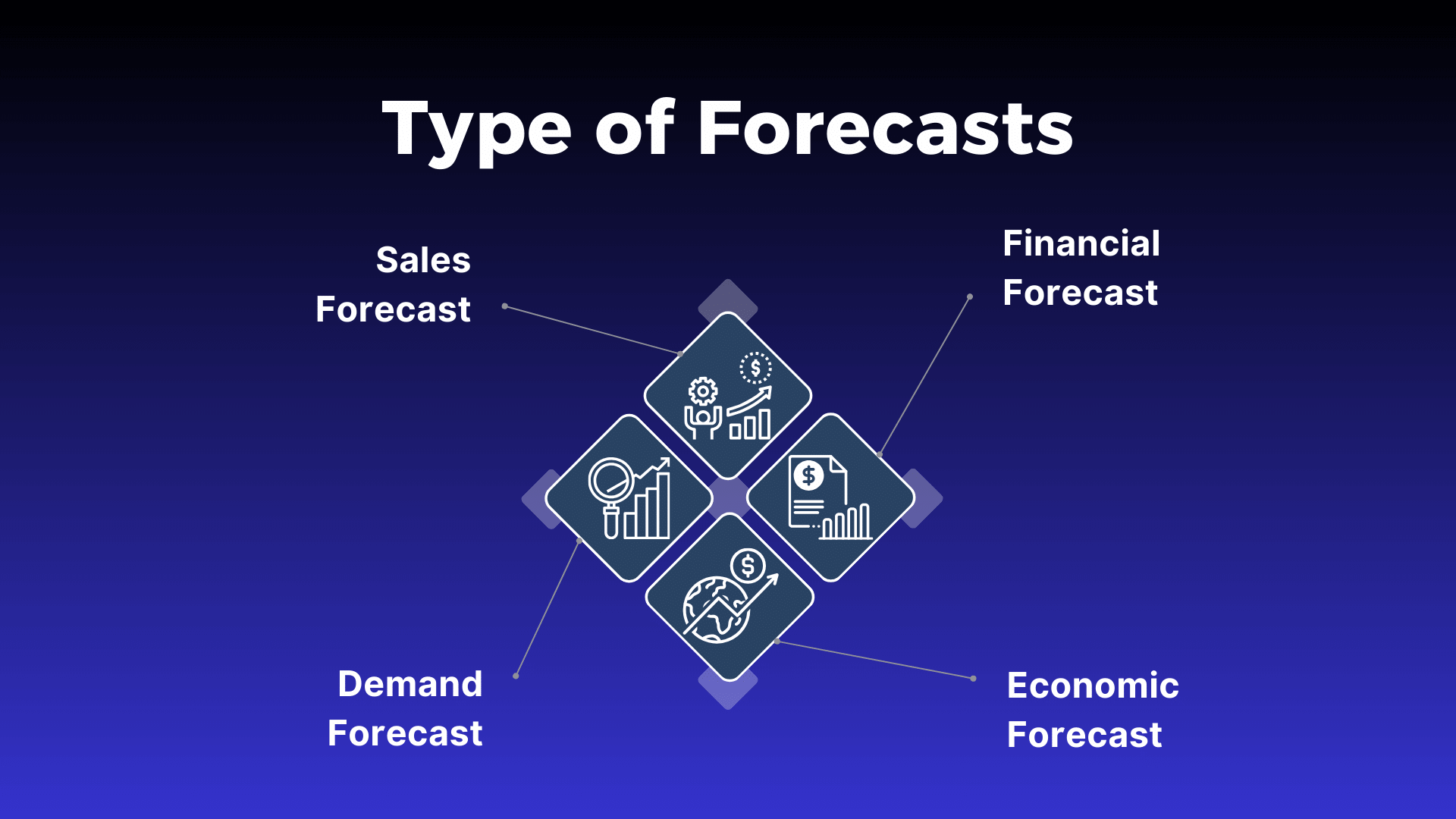

Types of Forecasts

Forecasts come in different forms, each tailored to specific purposes:

1. Sales Forecast

A sales forecast predicts future sales based on historical sales data, market research, and other relevant factors. It’s crucial for inventory management, production planning, and overall business strategy.

2. Financial Forecast

Financial forecasts focus on key financial metrics like revenue, expenses, and cash flow. They are commonly used for budgeting, financial planning, and investment decisions.

3. Economic Forecast

Economic forecasts analyse broader economic trends, such as inflation, interest rates, and GDP growth. They aim to anticipate how these factors may impact business operations.

4. Demand Forecast

Demand forecasts predict the demand for a product or service, enabling businesses to adjust production and inventory levels accordingly. These forecasts are essential for optimizing supply chains.

Key Differences: Budgeting vs. Forecasting

| Aspect | Budgeting | Forecasting |

|---|---|---|

| Purpose and Focus | Planning and controlling finances for a specific period, often a year. Sets targets and allocates resources to meet financial goals. | Predicting future financial outcomes, such as revenue and expenses. Provides insights for strategic decision-making and risk management. |

| Time Frame | Typically covers a fixed period, such as a fiscal year, and is usually updated annually or periodically. | Can cover both short-term and long-term horizons, depending on the specific forecast. Sales forecasts may be short-term, while financial forecasts can span several years. |

| Flexibility | Generally rigid, with limited flexibility to adapt to changing circumstances during the budget period. | More adaptable, allowing for scenario analysis and adjustments as new information becomes available. |

| Historical vs. Future-Oriented | Relies heavily on historical data and past financial performance as a basis for planning. | Emphasizes future-oriented analysis and predictions, often with a focus on emerging trends and market conditions. |

| Stake- holder | Primarily for internal use, guiding the allocation of resources within an organization. | May be used both internally and externally, serving as a basis for strategic decisions and investor relations. |

The Complementary Relationship: Budgeting and Forecasting

While budgeting and forecasting have distinct purposes, they are far from mutually exclusive. In fact, they complement each other in various ways:

1. Strategic Planning

- Forecasting provides the insights needed for strategic planning. For example, a sales forecast can inform the budgeting process by predicting future revenue.

2. Performance Evaluation

- Budgets establish performance benchmarks against which actual results can be compared. Forecasts can help adjust these benchmarks as new information becomes available, ensuring realistic targets.

3. Resource Allocation

- Budgets allocate resources based on predetermined goals. Forecasts help ensure that these allocations align with future financial expectations.

4. Risk Management

- Forecasts identify potential financial risks, while budgets outline strategies to mitigate those risks. Combining these approaches allows organizations to be proactive in managing uncertainties.

5. Continuous Improvement

- Regularly comparing budgeted figures with actual results and forecasts allows for continuous improvement in financial planning and decision-making. Lessons learned from these comparisons can inform future budgets and forecasts.

Conclusion: Embracing the Power of Budgeting and Forecasting

In conclusion, budgeting and forecasting are indispensable financial planning tools, each playing a unique role in the world of finance. Budgeting provides a structured approach to managing current finances, controlling spending, and achieving specific financial goals within a defined period. Forecasting, on the other hand, equips individuals and organizations with the ability to anticipate future financial outcomes, guiding strategic decisions and managing risks effectively.

Both processes are essential for individuals and businesses seeking to navigate the complexities of financial management. By understanding the differences and synergies between budgeting and forecasting, you can harness their power to make informed financial decisions and achieve long-term financial success. Whether you’re planning for personal financial excellence or steering a business toward prosperity, budgeting and forecasting are your trusted companions on the journey to financial success.

FAQ’s

- What is the core concept of budgeting and why is it important?

- Budgeting is the process of creating a financial plan for a specific period, helping individuals and organizations allocate resources efficiently and make informed financial decisions.

- What is the primary purpose of budgeting, and how does it help control spending?

- Budgeting helps control spending by setting limits on various expense categories, making it an essential tool for financial discipline.

- What is forecasting, and how does it differ from budgeting?

- Forecasting is the process of predicting future financial outcomes, while budgeting focuses on planning and controlling finances for a specific period.

- How do budgeting and forecasting complement each other in financial planning and decision-making?

- Budgeting sets performance benchmarks, while forecasting provides insights for strategic planning and risk management, making them valuable tools when used together.

Leave a Reply