In an era where speed and convenience reign supreme, the concept of embedded finance, often referred to as ‘EmFi,’ is making waves, albeit quietly, and revolutionising the way businesses operate. Embedded finance is now everywhere, touching everything from ordering food via mobile apps to requesting rideshares or making mobile payments.

Essentially, embedded finance represents the seamless integration of financial services into traditionally non-financial platforms. This integration includes services like lending, payment processing, and insurance, all seamlessly woven into the infrastructure of businesses traditionally unrelated to finance, presenting a truly game-changing solution.

Understanding Embedded Finance

Embedded finance allows non-financial entities to seamlessly incorporate financial services and products into their platforms using Application Programming Interfaces (APIs). For instance, imagine booking a flight and encountering an option to purchase insurance without leaving the booking app. This integration is just one facet of embedded finance. This article delves into the concept of embedded finance, with a particular focus on embedded lending.

The Many Faces of Embedded Finance

Embedded finance manifests in various forms. The key principle is to enable non-financial companies to offer financial services without redirecting customers to third-party websites. Examples include integrated insurance purchases, the “Buy Now Pay Later” (BNPL) trend in online retail, and platforms that integrate investment and trading services. Payment system integration is also common, with e-wallets embedded into e-commerce platforms.

Notably, major players, especially in the tech industry, are adding financial services as new verticals to their existing business models. This transformation has given rise to a new participant—the “enabler,” which bridges the gap between the marketplace and the financial services industry.

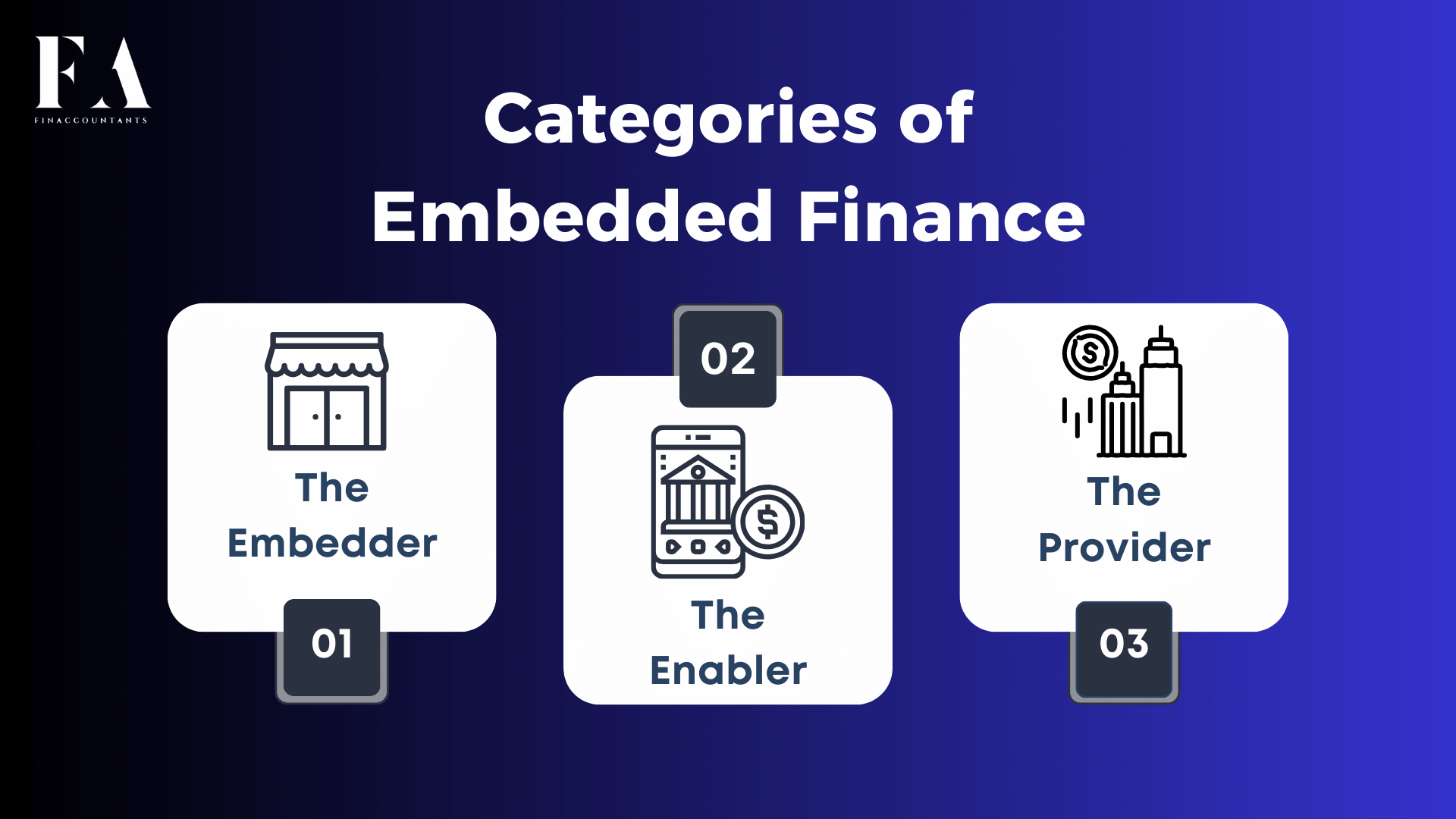

Key Categories of Embedded Finance

The embedded finance ecosystem is a complex network involving three key categories of participants, each playing a crucial role in delivering financial services to end consumers. Let’s delve into each of these categories to gain a deeper understanding:

- The Embedder: These are typically non-financial companies or platforms that integrate financial services into their core offerings. The embedders are the ones directly interacting with consumers and are responsible for making financial services seamlessly available within their existing products or services. For example, a ride-sharing app that offers riders the option to pay for their trips directly through the app is an embedder. By integrating payment processing, they enhance the user experience and add value to their core service.

- The Enabler: Enablers are the intermediaries that bridge the gap between the embedders and the providers of financial services. They provide the technological infrastructure, including APIs (Application Programming Interfaces) and other integration tools, that allow non-financial companies to easily incorporate financial services into their platforms. Enablers play a pivotal role in making embedded finance possible by simplifying the technical complexities and regulatory requirements associated with financial services integration. These entities may also offer compliance solutions and help embedders navigate the legal and regulatory landscape.

- The Provider: Providers are the financial institutions or entities that actually furnish the financial products or services embedded within non-financial platforms. They could be traditional banks, fintech startups, insurance companies, or lending institutions. Providers leverage enablers’ technologies to deliver their services to end consumers through embedders. For instance, a digital lending platform may partner with an e-commerce website (the embedder) to offer ‘Buy Now Pay Later’ (BNPL) financing options to customers during the online shopping experience. In this scenario, the digital lending platform is the provider.

Collectively, these three categories work in synergy to create a seamless and integrated financial experience for consumers. The embedders enhance their offerings, the enablers facilitate this integration, and the providers expand their reach and customer base by tapping into non-financial ecosystems. This collaborative ecosystem is redefining how financial services are accessed and consumed in today’s fast-paced digital world.

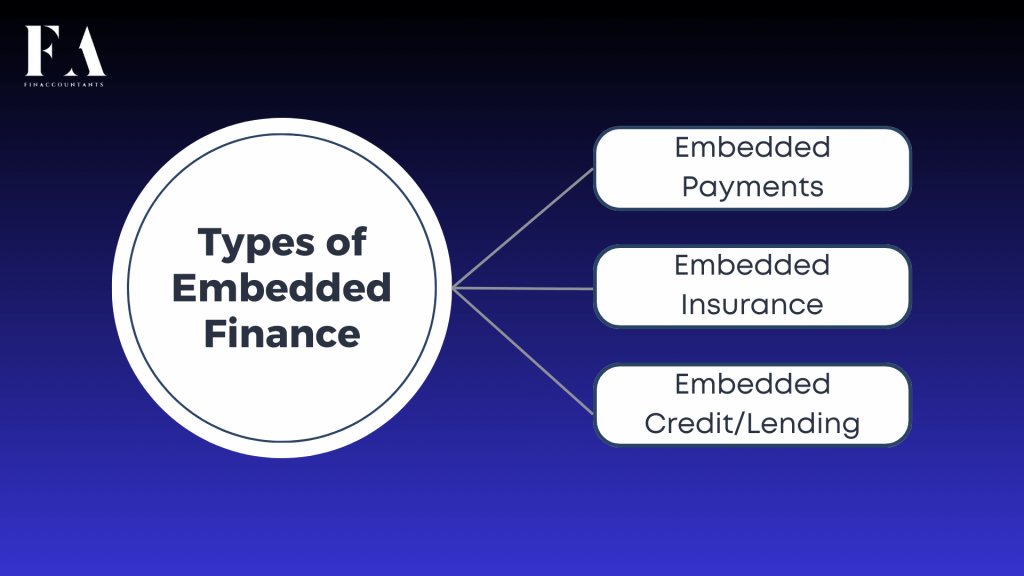

Types of Embedded Finance

- Embedded Payments: This is like having your wallet inside your favorite apps and websites. When you buy something online or in an app, you can pay for it right there, without needing to go to a separate payment website or take out your physical credit card. It’s as easy as clicking a button. This includes different ways to pay, like using credit cards, debit cards, or other online payment methods. For example, when you’re shopping online and you see the “Pay Now” button, you can complete your purchase without leaving the website or app.

- Embedded Insurance: Imagine if you could get insurance right when you need it, without going to a separate insurance company’s website. That’s what embedded insurance does. For instance, when you’re booking a flight or buying a new phone, you might see an option to get travel insurance or phone insurance right there. It’s super convenient because you don’t have to search for insurance providers separately. It’s like adding a protective shield to your purchases without any extra hassle.

- Embedded Credit/Lending: Have you ever seen the “Buy Now Pay Later” option when shopping online? That’s a form of embedded lending. It allows you to spread out your payments over time instead of paying for everything upfront. It’s a bit like getting a small loan for your purchase but without going to a bank. Equated monthly installments (EMI) work in a similar way. You can buy something and choose to pay for it in smaller chunks over several months. This makes big purchases more manageable and budget-friendly.

These embedded finance offerings are all about making your life simpler. They bring financial services right to the places where you need them the most, like when you’re shopping or booking flights. No more jumping between different websites or apps to manage your money – it’s all right there, integrated and hassle-free.

Advantages of embedded finance

For Businesses:

- Alternate Revenue Source: Embedded finance can create new income streams for businesses. For example, a retailer offering “Buy Now Pay Later” options can earn fees or interest on those payment plans.

- Competitive Advantage and Customer Loyalty: Businesses that offer embedded finance often stand out from competitors. Customers may prefer shopping where they can easily access financial services, leading to increased loyalty.

- Higher Order Value: Embedded finance can lead to larger purchases. Customers might buy more or choose higher-priced items when they have flexible payment options.

For Financial Institutions:

- Easier Customer Acquisition: Financial institutions can reach new customers by partnering with non-financial businesses. For instance, a bank partnering with a ridesharing app can acquire customers who might not have considered traditional banking services.

- Relevant Data Collection: With embedded finance, financial institutions can gather data from various sources, helping them better understand customer behavior and needs. This data can inform product development and marketing strategies.

- Easier Consumer Management: Embedded finance often involves seamless digital interactions, making it easier for financial institutions to manage customer accounts and provide support.

For Consumers:

- Convenience: The most apparent advantage for consumers is convenience. They can access financial services without leaving the platforms they use daily, making their lives simpler.

- Tailored Offerings: Embedded finance can offer tailored financial products. For instance, a food delivery app might suggest personalized insurance options based on a customer’s previous orders and preferences.

- Inclusion: Embedded finance can extend financial services to underserved populations, including those without traditional banking access.

- Better Overall Shopping Experience: With financial services integrated into shopping and other activities, consumers enjoy a smoother, more integrated experience. This can lead to increased satisfaction and trust.

Should Consumers Be Cautious About Embedded Finance?

Embedded finance aims to enhance accessibility and convenience for consumers, but it’s wise to exercise caution:

- Review Terms and Conditions Carefully: Before engaging in embedded finance services, it’s essential to read and understand the terms and conditions. These agreements outline how the services work, associated fees, and your rights and responsibilities.

- Compare Offerings in the Market: Take the time to explore the full range of offerings available in the market. Different providers may have varying terms, rates, or features. By comparing options, you can make informed choices that align with your needs.

- Be Mindful of Unintentional Purchases: The ease and speed of embedded finance can sometimes lead to unintentional purchases or commitments. Ensure that you’re aware of the financial implications of each action you take within embedded finance platforms.

By staying informed and cautious, consumers can enjoy the benefits of embedded finance while making responsible financial decisions.

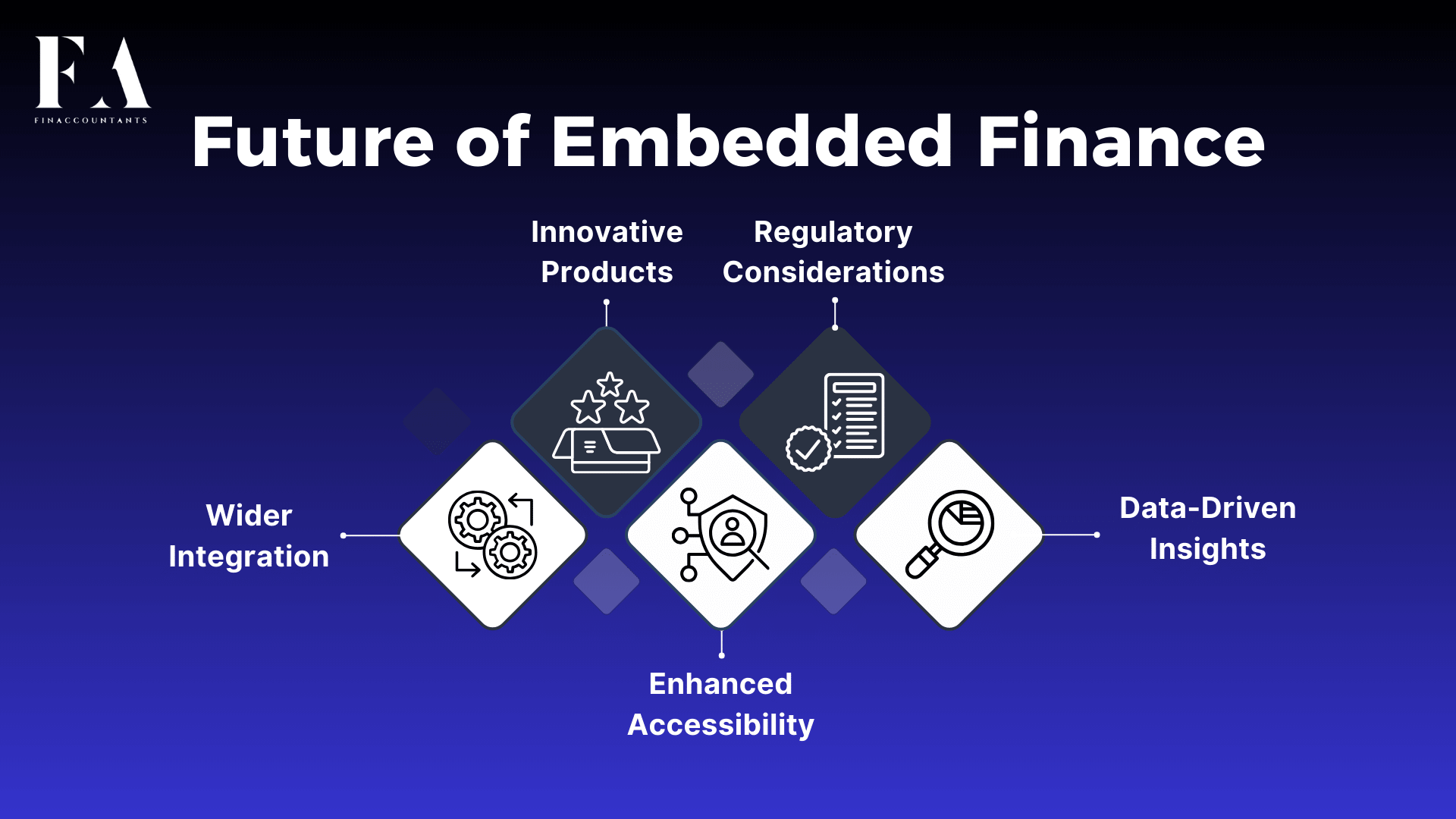

The Future of Embedded Finance

The future of embedded finance holds immense promise and potential. As technology continues to advance and consumer expectations evolve, we can anticipate several key developments:

- Wider Integration: One can anticipate even more widespread integration of financial services into various aspects of daily life. From healthcare to education and beyond, embedded finance will continue to expand its reach, making financial activities seamlessly integrated into every industry.

- Innovative Products: Fintech companies are constantly innovating, creating new and customized financial products. Embedded finance will likely give rise to a broader array of specialized offerings, catering to individual needs and preferences.

- Enhanced Accessibility: Embedded finance has the power to increase financial inclusion by reaching underserved populations. As it becomes more prevalent, it can provide previously excluded individuals with access to banking, lending, and investment opportunities.

- Regulatory Considerations: The growth of embedded finance will inevitably lead to regulatory scrutiny and the need for clear guidelines. Regulators will likely play an increasingly important role in shaping the industry to ensure consumer protection and fair practices.

- Data-Driven Insights: With the wealth of data generated by embedded finance transactions, businesses will gain deeper insights into consumer behavior. This data can be leveraged to provide more personalized and targeted financial services.

The Bottom Line

Embedded finance, or EmFi, represents a transformative shift in the way we interact with financial services. Its integration into various aspects of our daily lives promises greater convenience, accessibility, and customization.

As embedded finance continues to evolve and expand its presence, consumers should remain vigilant, carefully reviewing terms and conditions and making informed choices. While it offers substantial advantages, responsible usage is key to reaping its benefits.

The future of embedded finance is exciting, with the potential to enhance financial well-being and inclusivity for individuals and businesses alike. As it matures, it will undoubtedly shape the financial landscape in ways we can only begin to imagine. Embrace this revolution thoughtfully, and it can empower you to achieve your financial goals with unprecedented ease and efficiency.

FAQs

Q: How Does Embedded Finance Work?

A: Embedded finance involves integrating financial services seamlessly into non-financial platforms using Application Programming Interfaces (APIs). For example, when you see options to pay with a credit card or avail of insurance while making a purchase on a non-financial app, that’s embedded finance at work. These services are offered within the platform itself, creating a frictionless user experience.

Q: Is Embedded Finance Secure?

A: Security is a top priority in embedded finance. Businesses and financial institutions implementing embedded finance solutions adhere to rigorous security standards to protect user data and transactions. Encryption, authentication, and compliance with data protection regulations are some of the measures in place to ensure security.

Q: How Does Embedded Finance Benefit Small Businesses?

A: Embedded finance can be a game-changer for small businesses. It offers them easy access to financial services, including payment processing, lending, and insurance, without the need for extensive financial infrastructure. This can streamline operations, enhance customer experiences, and drive growth.

Q: What Are Some Emerging Trends in Embedded Finance?

A: Emerging trends include the expansion of embedded finance into new industries like healthcare and education, the rise of digital wallets and cryptocurrency integration, and the growth of AI-driven financial recommendations within non-financial apps.

Q: What Are the Regulatory Considerations for Embedded Finance?

A: The regulatory landscape for embedded finance varies by region and is evolving. Companies involved in embedded finance must comply with financial regulations and data protection laws. Regulatory bodies are actively monitoring this sector to ensure consumer protection and fair practices.

Q: How Will Embedded Finance Impact Traditional Banking?

A: Embedded finance is challenging traditional banking by offering more convenient and customer-centric financial services. While traditional banks are adapting by collaborating with fintech firms and enhancing their digital offerings, they also face competition from non-financial entities integrating financial services.

Q: Can Embedded Finance Help Improve Financial Inclusion?

A: Yes, embedded finance has the potential to improve financial inclusion by reaching underserved populations. Its convenience and accessibility can provide banking, lending, and investment opportunities to individuals and businesses that were previously excluded from the traditional financial system.

Q: What Are Some Examples of Innovative Embedded Finance Products?

A: Innovative embedded finance products include personalized microloans offered during online shopping, subscription-based finance for goods and services, and AI-driven financial advisors integrated into e-commerce platforms.

Leave a Reply