Tax planning is a process to meet tax obligations systematically and legally. Individuals can plan to lower the tax outflow with exempted allowances, deductions, and relief provided under the Income Tax Act.

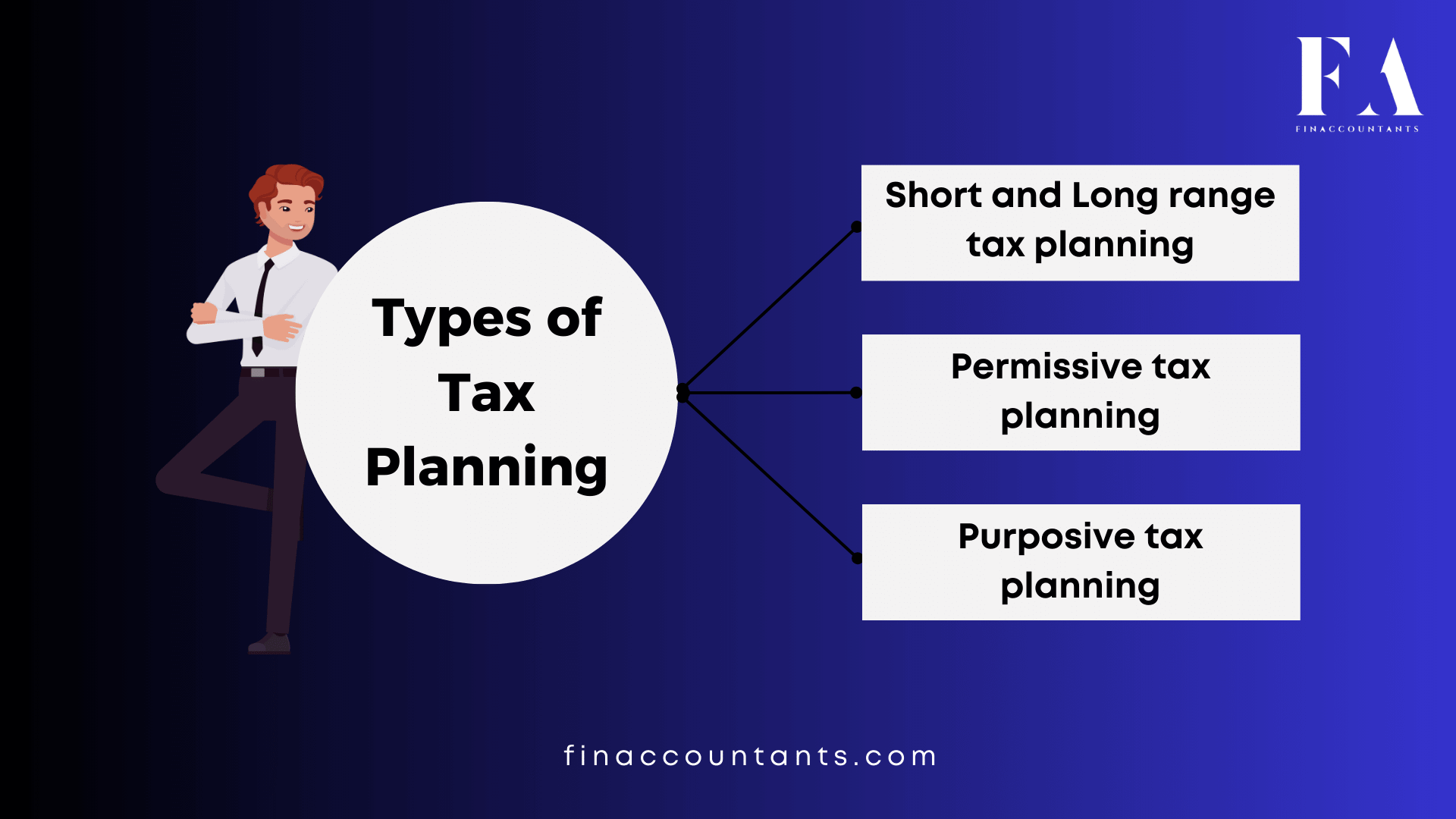

Type of Tax Planning

Following are some of the various methods of tax planning:

Short and Long range tax planning

Tax planning at the end of the fiscal year helps investors limit their legal tax liability and promotes substantial tax savings without long-term commitments.

A long-term tax planning plan established at the beginning of the fiscal year may not yield immediate benefits but can be beneficial in the long run.

Permissive tax planning

Indian tax planning involves utilizing various provisions of the Income Tax Act, 1961, including deductions, exemptions, contributions, and incentives on tax-saving instruments. For example, Unser section 80C provides various tax saving instruments.

Purposive tax planning

Purposive tax planning is tax-saver instruments to maximize investment benefits, including selecting appropriate investments, replacing assets, and diversifying assets based on residential status.

Process of Tax Planning

- Calculate your Gross Income

- Check your deduction and exemptions available as per Income Heads

- Invest to get deductions under chapter VIA

- Choose tax regime as per income and deductions

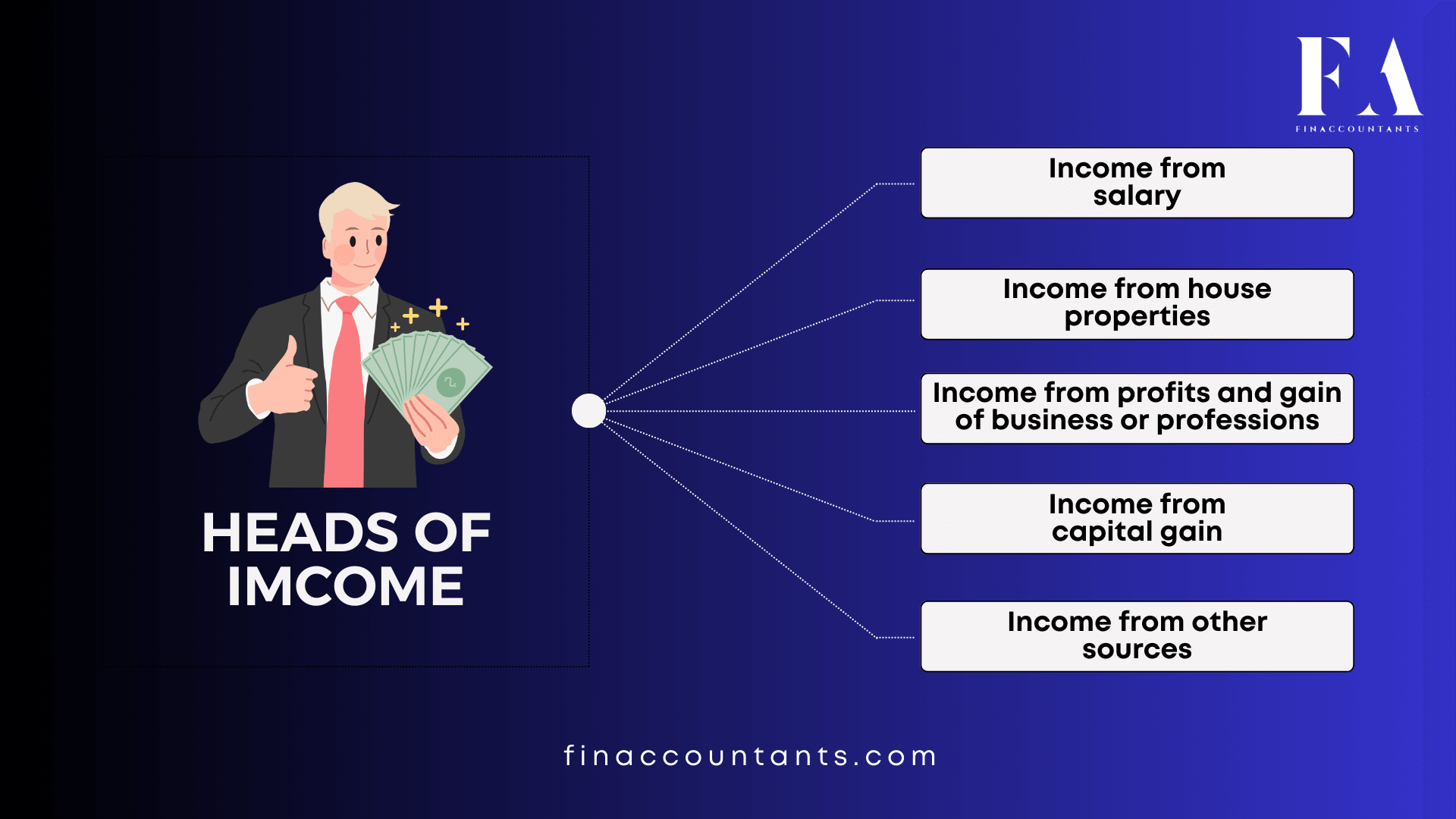

Heads of Income tax

The 5 heads of income are:

- Income from salary

- Income from house properties

- Income from profits and gain of business or professions

- Income from capital gain

- Income from other sources

1. Income from Salary

Salary Income refers to the compensation or earnings an individual receives from their employer in exchange for the work, Service, or employment they provide.

Tax can be saved with the following allowances:

Allowances

House Rent Allowance: The deduction available is the least of the following amounts:

- Actual HRA received

- 50% of (basic salary + DA) for those living in metro cities (i.e. Delhi, Kolkata, Mumbai or Chennai)

- 40% of (basic salary + DA) for those living in non-metros

- Actual rent paid (-) 10% of basic salary + DA

Leave travel allowance: When you travel for pleasure, whether by yourself or with friends or relatives, you must pay a leave allowance. As it is paid, it is twice tax-free for a period of four years.

Medical allowance: Rs. 15000 per annum is exempted under medical allowance.

Conveyance allowance: Upto Rs.800 per month can be claimed as exemption under this head.

Food Coupons: You might receive lunch coupons from companies like Sodexo from your job. These food coupons are taxable as a perk in the employee’s hands. However, 2 meals for a day of Rs. 50 each is exempted from taxes.

- The working day for exempted meals are considered 22 days in a month and 2 meals a day can save Rs. 2,200 in a monthly (22*100).

- Consequently, the yearly exemption will be Rs 26,400.

Children Allowances: Your employer might include an education allowance in pay for your kids. The employer is not required to pay taxes on any educational benefits they get. However, the employee can only request an exemption of up to Rs. 100 per month or Rs. 1,200 per year. There is a two-child limit on the exemption.

2. Income from House Property

The Income Tax Act outlines the taxation policy on house property, defining ‘self-occupied’ and ‘let out’. If a taxpayer owns multiple self-occupied houses, only two are treated as single self-occupancy property, while the rest are let out.

Deduction allowed under the Head

- U/s 24a 30% of Rental Income can be claimed as standard deduction,

- U/s 24b the deduction is allowed for interest on home loans (if any), and

- Deduction for municipal taxes paid are also deductible under this head of income.

3. Income from Profits and Gain of Business or Profession

The Income Tax Act taxes profits from import sales, incentives, interest, salary, bonuses, and firm commissions.

The few types of income that are chargeable under this head of income are:

- Profits earned from the sale of a certain license

- Gains earned by the business during an financial year

- Cash received on the export of Services

- Salary, Profit, Bonus received from Partnership firms

Presumptive Income

Presumptive Income Tax under Section 44AD- Business Income

The individual can choose the presumptive income tax scheme under section 44AD. The followings are allowed to adopt 44AD:

- Individual Resident of India

- Hindu Undivided Family, Karta should be Resident of India

- Partnership Firm (not Limited Liability Partnership Firm)

- Persons / Business not covered under this section 44AD

44AD is a scheme to give relief to individuals or small business except:

- Income earned from plying, hiring or leasing of goods carriages referred to in section 44AE.

- The income earned from nature of business of commission or brokerage

- The assessee whose total turnover or gross receipts for the year exceed Rs. 2,00,00,000.

- A assessee carrying on profession as mentioned Section 44AA(1) does not qualify for the presumptive taxation scheme.

- Tax Liability under section 44AD presumptive taxation scheme

In case of a person declaring Income under the provisions of 44AD, taxable income would be 8% on turnover if payments are accepted in cash mode or 6% of the turnover if payments are accepted digitally. However, assessee can declare income more than 8% or 6%, of turnover on voluntarily basis.

Professional Income – Presumptive Income Tax under Section 44 ADA

A Residential person engage in following professions can declare of presumptive taxation scheme of section 44ADA:

- Medical Services

- Legal Services

- Engineering or architectural Services

- Accountancy Services

- Technical consultancy

If gross receipt from profession exceed Rs. 50,00,000 in a financial year Professionals cannot to choose this section.

NOTE: In Budget 2023 the threshold u/s 44ADA is increased from 50,00,000 to Rs 75,00,000 but the cash receipts should be less than 5% as per the requirement.

- Tax Liability under Section 44 ADA

In case of a assessee adopted the provisions of section 44ADA, taxalbe income will be calculated as 50% of the total gross receipts of the profession on presumptive basis.

Income Tax under Section 44 AE

The presumptive taxation scheme under section 44AE can be adopted by a individual, firms, company etc. who has the business of hiring, plying, or leasing of goods carriages

subject to the vehicle owned should not be more than 10 goods vehicles at any time during the year.

- Tax liability under section 44AE

In case of a person choosed for the presumptive taxation scheme U/s section 44AE, income will be computed as per the formula available for Section 44AE

4. Income from Capital Gains

The Income Tax Act taxes income from capital assets, divided into long-term and short-term gains. Long-term capital gains (LTCG) are taxed at 20%, while short-term gains are taxed at 15%. Securities are taxed at 15% if sold within 36 months, and 12 months from the purchase date.

Capital gain exemptions

Capital gain exemption can be claimed U/s 54, 54B, 54D, 54EC, 54ED, 54F, 54G, or 54GA.

Under Section 54

- The individual or HUF has long-term capital gain through sale of a residential property, is exempted to the degree that it is invested in the

- Another residential property must be acquired within 1 year before or 2 years after transferring the property.

- Residential house construction must be completed within 3 years of transfer.of property

Section 54EC: Old Asset: Any Asset, New Asset: Specified Bonds

The assessee can claim a deduction under section 54EC by investing the capital gain in specified long-term assets.bonds as announced by the government within six months from transfer of property.

Section 54F: Old Asset: Any Asset, New Asset: Residential House

- Any Gain arising by an individual or HUF from the sale of any Long Term Asset other than Residential Property shall be exempt full, if the entire net sales consideration is invested in.

- Any A residential house must be purchased within 1 year before or 2 years after the property transfer. assets or

- A residential house must be constructed within three years of the stated timeframe. transfer of such property

5. Income from Other Sources

Income from sources outside the four heads falls under this category. from other sources.

Section 56(2) of the Income Tax Act lists the incomes taxable under the head of Income from Other Sources.Some of these incomes include:

- Dividend income

- Interest income

- Family pension income

- Gifts received

- Royalty income

Deductions under Chapter VI A of Income Tax Act

Chapter VI A of the Income Tax Act allows assessees to claim deductions from gross total income for tax-saving investments, permitted expenditures, and donations.

The Chapter VI A of Income Tax Act provide the following sections:

80C: Deduction of premium paid for life insurance premium, deferred annuity, Principal payment for House Loan, contributions to provident fund (PF), Contribution to specified Mutual Funds, subscription to certain equity shares or debentures, Sukanya Samriddhi account etc. The maximum deduction limit is Rs 1,50,000 put together with section 80CCC and section 80CCD(1).

80CCC: Deduction can be claimed for certain pension funds. The deduction limit is Rs 1.5 lakh together with section 80C and section 80CCD(1).

80CCD(1): Deduction allowed

Central Government, an employee can enjoy a tax exemption of 10% of their salary (Basic+DA). For non-employees, a tax exemption of 20% of their gross total income in a financial year is applicable. The total limit for tax exemption is Rs 1.5 lakh, which includes 80C and 80CCC.

80CCD(1B): Deduction up to Rs 50,000 is allowed for contribution to pension scheme of Central Government (NPS) can be claimed.

80CCD(2): Deduction is allowed for contribution to pension scheme of Central Government by employer. Tax benefit is available 14 per cent contribution by the employer, where contribution made by the Central Government and where contribution made by any other employer, tax benefit will be 10 per cent.

80D: Health Insurance Premium paid by individuals other than senior citizens eligible for deduction up to Rs 25,000. For senior citizens, the deduction can be claimed up to Rs 50,000 and maximum deduction can be clamied u/s 80D is Rs 1,00,000.

80DD: Maintenance expenses for dependent disabled person including medical treatment can be claimed as deduction up to Rs 75,000.

80DDB: Deduction for expenditure up to Rs 40,000 on medical treatment of specified disease from an oncologist, a urologist, a haematologist, an immunologist, a neurologist,or other specialist, as prescribed by Government.

80E: Deduction can be clamied for interest on loan for higher education without any upper limit.

80EE: Deduction can be clamied for interest on loan for residential house property up to Rs 50,000.

80EEA: Deduction can be clamied for interest on loan take for certain house property up to Rs 1,50,000 (on affordable house).

80EEB: Deduction can be clamied for interest on loan for purchase of electric vehicle up to Rs 1,50,000.

80G: Donations made to certain funds, charitable institutions, etc. The percentage of deduction depends on the nature of the donee, the eligibility can be 100 per cent of total donation made during the year, 50 per cent of total donation or 100 per cent of donation with a cap of 10 per cent of adjusted gross income during the year.

80GG: Deductions for rent paid by non-salaried individuals who don’t get HRA benefits. Deduction can be claimed for Rs 5,000 per month or 25 per cent of total income in a year, whichever is less.

80GGA: Donations for scientific research or rural development are fully deductable.

80GGC: Donation made to Political parties are fully deductible, provided such donations are non-cash donations.

80TTA: Interest income from Saving Bank account upto Rs 10,000 can be claimed as deduction by assessees other than Resident senior citizens.

80TTB: Deductions can be claimed for Rs. 50,000 for interest income from deposits in case of Resident senior citizens.

80U: Deduction in this section can be claimed upto Rs. 1,25,000 depends on type and extent of disability.

Tax Regime

For the FY 2022-23 (AY 2023-24)

| Income Slabs | New Tax Regime |

| ₹0-₹2,50,000 | NIL |

| ₹2,50,000-₹5,00,000 | 5% (Tax Rebate is available u/s 87A) |

| ₹5,00,000-₹7,50,000 | 10% |

| ₹7,50,000-₹10,00,000 | 15% |

| ₹10,00,000-₹12,50,000 | 20% |

| >₹15,00,000 | 30% |

Here are the income tax slabs for individuals below 60 years of age and HUF:

| Income Slabs | New Tax Regime |

| Up to Rs 2,50,000 | NIL |

| ₹2,50,000-₹5,00,000 | 5% |

| Rs 5,00,000 – Rs 10,00,000 | 20% |

| >₹10,00,000 | 30% |

Comparison of tax rates under New tax regime & Old tax regime for FY 2022-23 (AY 2023-24)

| Old Tax Regime | New Tax Regime | |||

| Slabs | < 60 years of age & NRIs | > 60 to < 80 years | > 80 years | FY 2023-24 |

| ₹0 – ₹2,50,000 | NIL | NIL | NIL | NIL |

| ₹2,50,000-₹3,00,000 | 5% | NIL | NIL | NIL |

| ₹3,00,000-₹5,00,000 | 5% | 5% (tax rebate u/s 87A is available) | NIL | 5% |

| ₹5,00,000-₹6,00,000 | 20% | 20% | 20% | 5% |

| ₹6,00,000-₹7,50,000 | 20% | 20% | 20% | 10% |

| ₹7,50,000-₹9,00,000 | 20% | 20% | 20% | 10% |

| ₹9,00,000-₹10,00,000 | 20% | 20% | 20% | 15% |

| ₹10,00,000-₹12,00,000 | 30% | 30% | 30% | 15% |

| ₹12,00,000-₹12,50,000 | 30% | 30% | 30% | 20% |

| ₹12,50,000-₹15,00,000 | 30% | 30% | 30% | 20% |

| >₹15,00,000 | 30% | 30% | 30% | 30% |

Important points to note if you select the new tax regime:

- The tax rates will be same for all categories (i.e. Individuals, Senior Citizen and Super Senior Citizen) in the New tax regime.

- In Budget 2023, rebate under new regime has been increased and therefore, income upto Rs 7 lakh will be tax-free from FY 2023-24.

- Surcharge: In case the income exceeds a certain threshold, surcharge will be applicable

- Surcharge rates are as below:

- 10% of Income tax if total income > Rs.50 lakh

- 15% of Income tax if total income > Rs.1 crore

- 25% of Income tax if total income > Rs.2 crore

- 37% of Income tax if total income > Rs.5 crore

Conditions for opting new tax regime

The New Tax regime’s concessional rates require taxpayers to give up previously accessible exemptions and deductions, with a total of 70 deductions affected.and exemptions that are prohibited, with the most popular ones mentioned below:

| Particulars | Old Tax Regime | New Tax regime | New Tax Regime |

| (until 31st March 2023) | (From 1st April 2023) | ||

| Income level for rebate eligibility | ₹ 5 lakhs | ₹ 5 lakhs | ₹ 7 lakhs |

| Standard Deduction | ₹ 50,000 | – | ₹ 50,000 |

| Effective Tax-Free Salary income | ₹ 5.5 lakhs | ₹ 5 lakhs | ₹ 7.5 lakhs |

| Rebate u/s 87A | 12,500 | 12,500 | 25,000 |

| HRA Exemption | ✓ | X | X |

| Leave Travel Allowance (LTA) | ✓ | X | X |

| Other allowances including food allowance of Rs 50/meal subject to 2 meals a day | ✓ | X | X |

| Standard Deduction (Rs. 50,000) | ✓ | X | ✓ |

| Entertainment Allowance and Professional Tax | ✓ | X | X |

| Perquisites for official purposes | ✓ | ✓ | ✓ |

| Interest on Home Loan u/s 24b on slef-occupied or vacant property | ✓ | X | X |

| Interest on Home Loan u/s 24b on let-out property | ✓ | ✓ | ✓ |

| Deduction U/s 80C( EPF/LIC/ELSS/PPF/FD/Children’s tutution fee etc) | ✓ | X | X |

| Employee’s (own) contribution to NPS | ✓ | X | X |

| Employer’s contribution to NPS | ✓ | ✓ | ✓ |

| Medical insurance premium – 80D | ✓ | X | X |

| Disabled Individual – 80U | ✓ | X | X |

| Interest on education loan – 80E | ✓ | X | X |

| Interest on Electric vehicle loan – 80EEB | ✓ | X | X |

| Donation to Political party/trust etc – 80G | ✓ | X | X |

| Savings Bank Interest u/s 80TTA and 80TTB | ✓ | X | X |

| Other Chapter VI-A deductions | ✓ | X | X |

| All contributions to Agniveer Corpus Fund – 80CCH | ✓ | Did not exist | ✓ |

| Deduction on Family Pension Income | ✓ | ✓ | ✓ |

| Gifts up to Rs 50,000 | ✓ | ✓ | ✓ |

| Exemption on voluntary retirement 10(10C) | ✓ | ✓ | ✓ |

| Exemption on gratuity u/s 10(10) | ✓ | ✓ | ✓ |

| Exemption on Leave encashment u/s 10(10AA) | ✓ | ✓ | ✓ |

| Daily Allowance | ✓ | ✓ | ✓ |

| Transport Allowance for a specially-abled person | ✓ | ✓ | ✓ |

| Conveyance Allowance | ✓ | ✓ | ✓ |

Conclusion

It’s important for individuals to understand the tax implications of their salary structure and make informed decisions regarding investments, deductions, and the choice of tax regime. Consulting a tax advisor or financial planner can be beneficial in optimizing their tax planning strategies while staying compliant with tax laws.

Leave a Reply