Tax planning is an activity undertaken by a taxpayer in order to reduce the amount of tax owed to him or her by maximizing the use of all available deductions, allowances, exclusions, and other legal provisions. In other words, it’s the examination of a financial situation through the lens of taxation. The goal of tax planning is to make sure that taxes are as efficient as possible. Corporate Tax planning ensures that all aspects of the financial plan work together to achieve maximum tax efficiency.

For fiscal effectiveness, corporate tax planning is essential. The tax liability was decreased, and retirement plans were able to be used to their full potential.

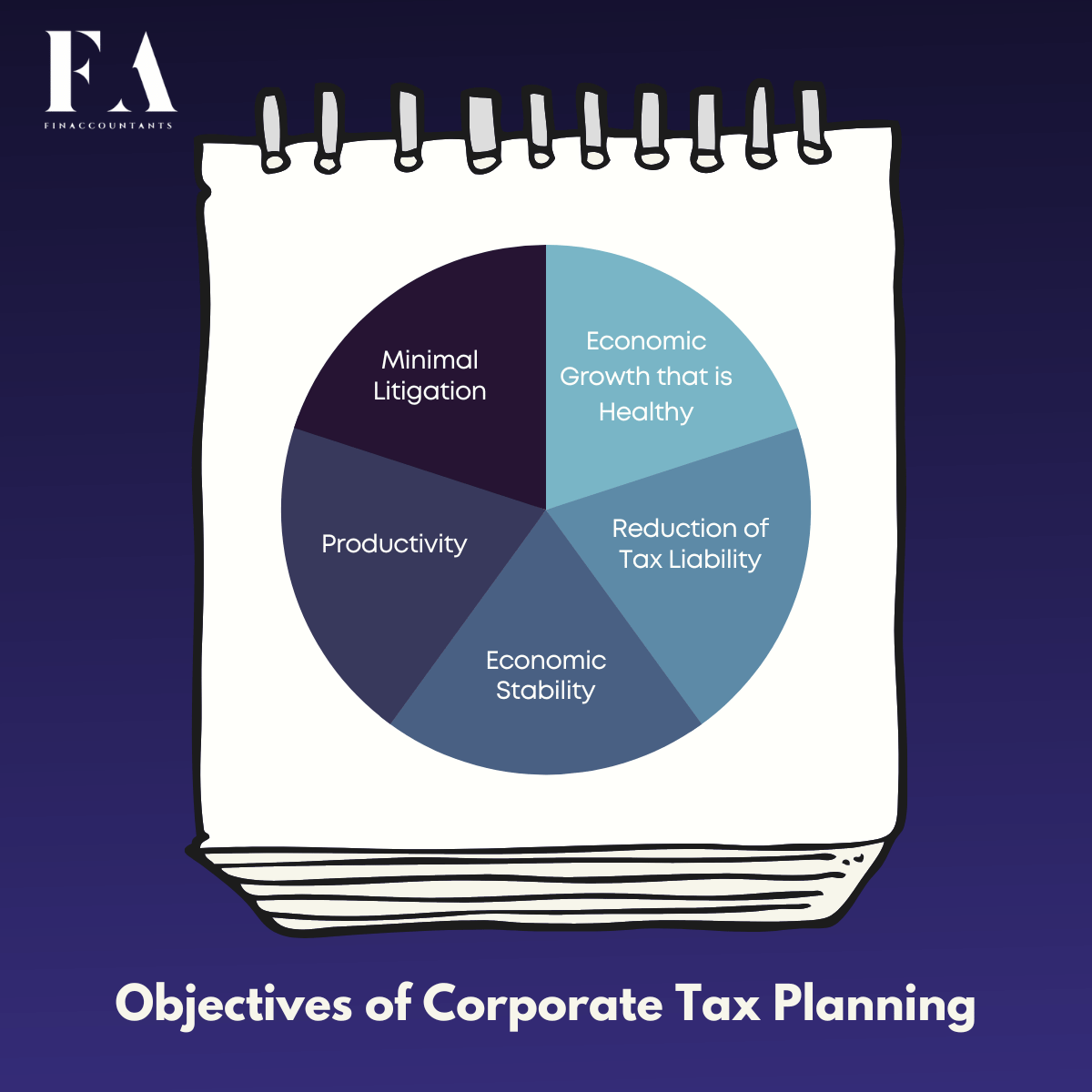

Objectives of Corporate Tax Planning

The objectives of Corporate Tax Planning are as follows-

1. Minimal Litigation

There is always a conflict between the tax collector and the taxpayer. In such a case, it’s critical that tax payment compliance is followed and correctly utilized to keep friction to a minimum.

2. Productivity

Channeling taxable income to various investment plans is one of the most significant goals of tax planning.

3. Reduction of Tax Liability

Making sure your company is legally compliant and correctly managed will help you as a taxpayer save the maximum money on your tax payment.

4. Economic Growth that is Healthy

An economy’s growth is largely determined by the growth of its citizens. Tax planning forecasts the development of free-flowing white money.

5. Economic Stability

When a business’s tax planning is done properly, it adds to its stability.

Types of Corporate Tax Planning

There are two types of distances: short-range and long-range. Tax Planning: Short-range tax planning is tax planning that is done once a year to achieve certain goals. Long-term tax planning, on the other hand, excludes any type of quick payment.

1. Permissive Tax Planning

This type of planning adheres to tax laws.

2. Purposive Tax Planning

This is a tax planning strategy that takes the use of legal loopholes.

Tax planning refers to the methodical application of tax regulations in order to properly manage a person’s tax burden. Leading to the receipt of tax advantages in line with the law and in the nation’s and people’s best interests.

India’s Corporate Tax Planning

Indian law provides a wide range of tax-saving alternatives for taxpayers, including a huge number of exclusions and deductions via which you can reduce your overall tax burden.

- Eligible taxpayers can take advantage of the deductions found in Sections 80C through 80U.

- All of these deductions are made against the amount of tax owed.

- Other provisions of the Income Tax Act of 1961, such as exemptions and tax credits, can help you reduce your tax liabilities.

Corporate Tax Planning

This is a method of reducing a registered company’s liabilities. One of the most common techniques is to include deductions for company transportation, employee health insurance, and so on. Your company can legally decrease its tax burden by taking advantage of tax deductions and exclusions offered under the Income Tax Act of 1961.

As a company’s profits grow, so do its tax bills. In this circumstance, it is critical that they devote sufficient effort to tax planning that minimizes liabilities. At the time of inflation, a tax plan reduces both direct and indirect taxes. This isn’t all.

Tax planning entails the careful preparation of:

- Expenses.

- Budget for capital expenditures

- Costs of sales and marketing.

The following factors contribute to effective corporate tax planning:

- To receive tax benefits, all you have to do is invest in qualified securities.

- Providing accurate information to the appropriate IT authorities.

- Being well-versed in the appropriate tax laws as well as judicial rulings on the subject.

- Tax planning should be done entirely within the bounds of the law.

- Business objectives should be considered, as well as the flexibility to accommodate future changes.

- You may be a long-time taxpayer or a first-time payer, but if you did not correctly plan your taxes, you are likely paying more tax than you should.

This is the organization of a taxpayer’s business or financial activities in such a way that the entire tax benefit can be obtained through legal means, resulting in the lowest possible tax amount.

People make a lot of blunders when it comes to taxes

1. Procrastination

As a tax planner, this is the source of all your blunders. Instead of making timely investments that lead to optimal tax planning, this will eventually lead to you paying more taxes.

2. Investing in insurance products to save money on taxes

Many of us receive phone calls from insurance firms as the end of the fiscal year approaches, urging us to purchase a tax-saving insurance policy. This isn’t the best course of action.

The income tax provisions appear to be so complicated that the average person avoids dealing with them.

3. Compounding power through tax-advantaged mutual funds

Despite all of the evidence, many people overlook the potential of compounding.

4. Failure to take advantage of all available tax-saving options

Don’t be like those people who think tax planning begins and stops with Section 80C of the Income Tax Act of 1961, which exclusively covers investment instruments for tax savings.

Conclusion

The analysis of a financial position or plan to ensure that all parts work together to allow you to pay the least amount of taxes feasible is known as tax planning. Efficient Corporate Tax planning is defined as a strategy that reduces the amount of money you pay in taxes. Individual investors’ financial plans should include tax planning as a key component. Success hinges on lowering one’s tax liability and increasing one’s ability to contribute to retirement programs. FinAccountants can provide you with more information.

Leave a Reply